![]() Why doesn’t CarFax provide alerts for potentially troubling car history data, or provide a score based on the vehicle history? Like many business decisions, there are several contributing factors and, in this case, each should make car buying consumers question the value of the report and whether CarFax has their best interests in mind. Indeed, the same factors may even open an opportunity for a more nimble competitor to rethink the market, rebuild the reports and redesign the industry.

Why doesn’t CarFax provide alerts for potentially troubling car history data, or provide a score based on the vehicle history? Like many business decisions, there are several contributing factors and, in this case, each should make car buying consumers question the value of the report and whether CarFax has their best interests in mind. Indeed, the same factors may even open an opportunity for a more nimble competitor to rethink the market, rebuild the reports and redesign the industry.

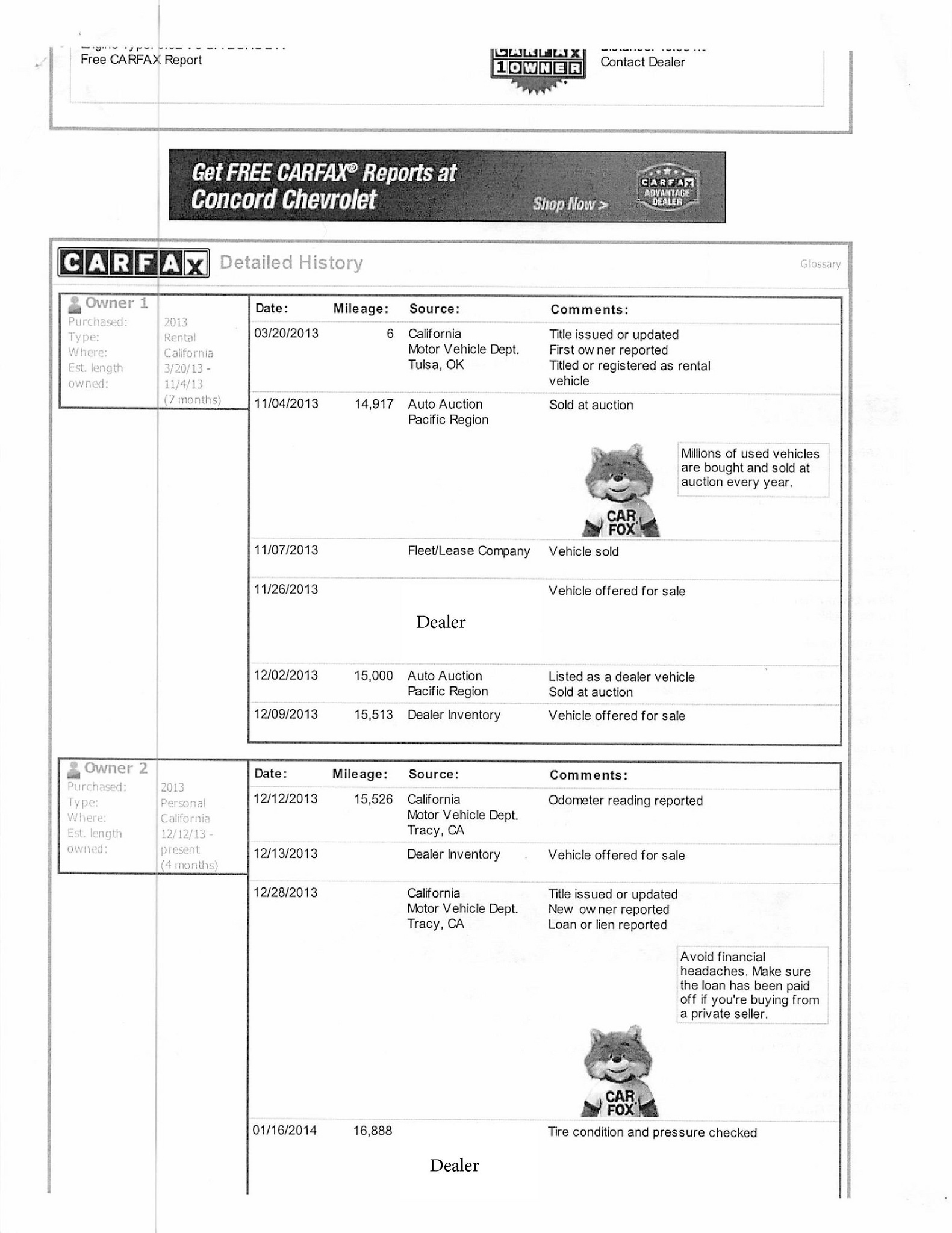

The car-buying public is not CarFax’s primary customer. CarFax—which controls an estimated 90% of the auto title history market—built its empire by penning exclusive agreements with numerous auto manufacturers and their certified pre-owned programs, as well as auto classified outfits such as Auto Trader and Cars.com. The vast majority of CarFax reports are purchased by the people certifying or selling used cars, and then provided to the buying public for free. Why? Because a clean CarFax report provides a consumer confidence that they are getting what they pay for. As we saw in yesterday’s posts here and here, however, the CarFax report offers only raw data, no analysis, and the consumer’s confidence is not always earned.

The fact is, CarFax’s primary customers like the reports minimal. CarFax specifically calls out only the worst case cars (such as titles branded Salvage or Flood), which smoothes the sales process and provides consumers with a perception of quality despite minimal due diligence and no analysis. To this end, CarFax is not truly a research tool for consumers, but a sales tool designed to reduce friction in the used car market. If CarFax went out of its way to raise flags for questionable history, the pool of purchasers for the car would diminish as would the value of the car. If CarFax provided a score, its dominance in the market would likely set up de facto diminishing tiered pricing based on the score range, and likely give more false positives than negatives. As it is, if a CarFax shows a title branded as Salvaged or Flood, the car’s resale value is almost nothing. If CarFax provided a more robust title history analysis, the first casualty would be the bottom line of their best customers.

Interestingly enough, auto dealerships—who are begrudgingly one of CarFax’s primary customers— have recently come out against CarFax reports as unreliable. The most public outcry is voiced in an antitrust lawsuit (Maxon Hyundai Mazda NYLSI Inc. d/b/a/ Sunrise Toyota et al. v. CarFax Inc., case number 13-cv-2680, in the U.S. District Court for the Southern District of New York) currently supported by nearly 600 dealerships around the country. While dealerships certainly stand to gain from the lack of analysis in CarFax reports, that benefit appears outweighed by the squeeze put on dealers resulting from CarFax’s sweetheart deals with OEMs, certified pre-owned programs and auto classifieds. With each of those entities only recognizing CarFax reports, the suit alleges CarFax often charges dealers five times as much as competing title history providers. In the effort to unseat CarFax from this alleged monopoly, consumers have found an unlikely ally in the dealers who now claim CarFax reports are unreliable and subject dealers to unnecessary litigation. Whether the dealer’s arguments find traction is yet to be seen, but in the meantime, have no doubt that despite their protests, dealers will milk as much value from the shroud of quality CarFax confers.

In all of this, the consumer gets lost, both figuratively and literally. The reports are not the best product for consumers, but are instead designed to facilitate sales. The reports also provide raw data with no analysis. While many consumers will meaningfully interpret the data, many more will see the lack of obvious alerts as a stamp of approval. It would be no easy feat to develop an algorithm to detect questionable data in a title history and thus provide meaningful analysis, but not impossible. Through their antitrust claims discussed above, hundreds of dealerships are unwittingly creating a market for precisely such a product. Indeed, from a public relations and litigation perspective, dealerships (and OEMs to some degree) could benefit from helping support or design a product which ensures transparency in auto deals, and would likely see a decline in auto fraud litigation costs as a result. Even better, if a title-history product had organic growth based on consumer transparency creating mutual benefit to consumer and business alike, the sheen of CarFax’s gold-standard perception would fade, and the gravity of exclusivity agreements diminish.

Certainly this article does not cover the title history industry with sufficient depth, and the solution proposed above is oversimplified; however the point is that consumers and industry need not accept the status quo. The innumerable lawsuits filed by consumers for defects in cars hidden or undisclosed in title reports coupled with the antitrust lawsuit by dealers reveal the title history industry as broken, or at the very least damaged. Given that rare agreement by major players on both sides of such a common, yet critical transaction, there is no question this industry is ready for redesign.

Rocky’s comments

This is the same problem with investment analysts and accounting firms. Accounting firms are audited by the people who pay them, not an independent third party. Part of the reason that Groupon’s S-1 filing was so full of flaws was that Ernst & Young was being paid by Groupon. Keeping the customer happy comes into play.